One Stop Systems (OSS)

OSS stock analysis: Net-cash defense AI play up 89% YoY. Why I sold after hitting target, plus full breakdown of financials & growth drivers.

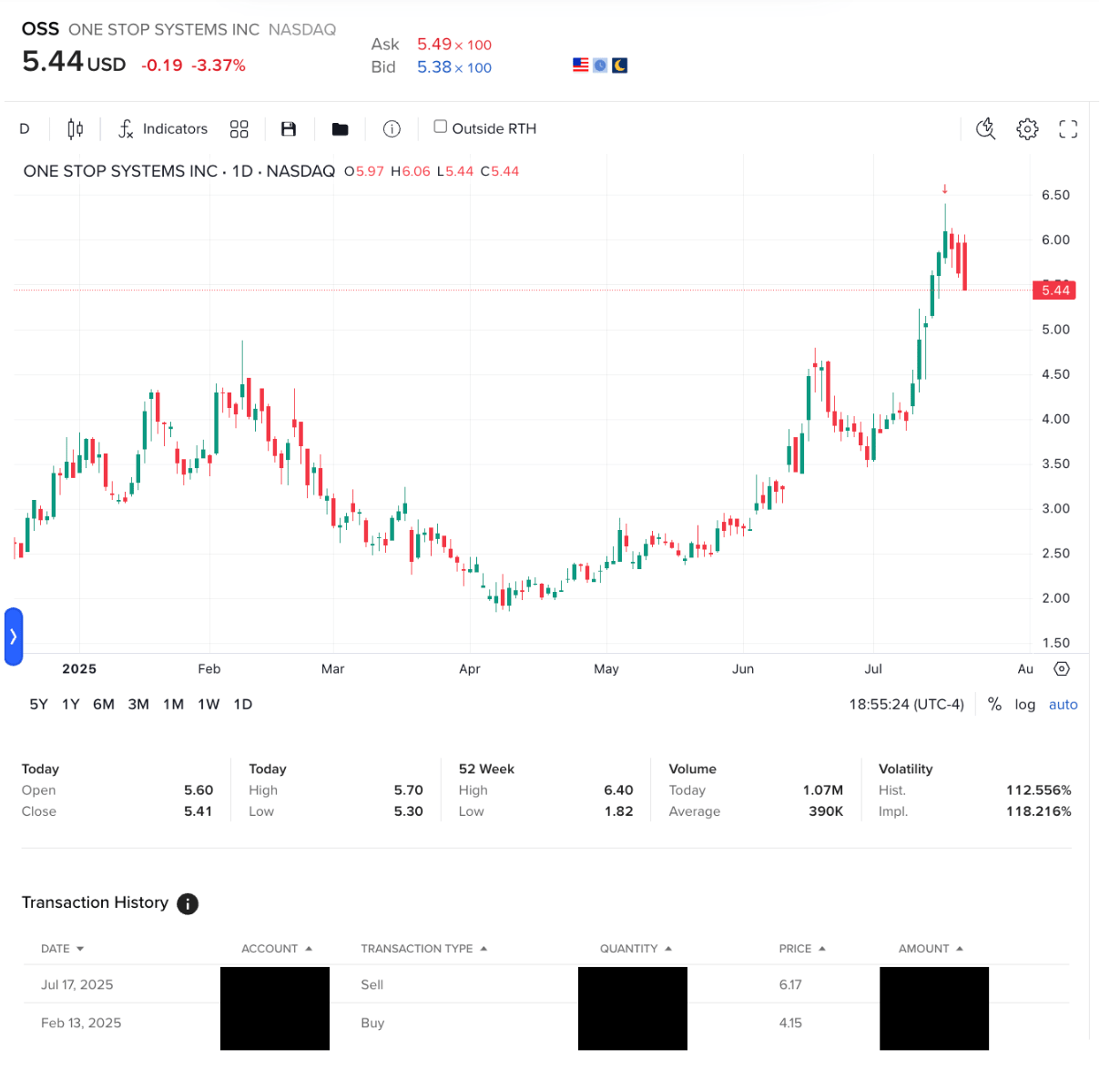

For context, I have had this post sitting in drafts for a long time (about a week after I wrote my first piece on GSIT) but I didn't know what exactly I wanted to do with the analysis and write-ups. Unfortunately, within that time the stock ran up past my near-term price target, and I closed the trade. I am letting it breathe a bit now, though I still believe in its long-term value (transactions below).

One Stop Systems (OSS)

One Stop Systems (OSS) is a net-cash microcap building the “rugged edge data center” for defense and industrial AI.

Financial Performance

Revenue Milestones

In 2022, OSS’s revenue was $72.4 million, a 17% increase from the prior year (2021).

2023 saw revenues decline 15.9% to $60.9 million. This was mainly due to a major media customer winding down its program. Without that customer, revenue would have grown about 4% year over year.

In the first nine months of 2024, sales dipped 17% to $39.6 million, still feeling the pinch from the media customer’s exit and softer demand in Europe.

Margin Expansion

Gross margins have hovered in the high 20s to low 30s. In 2023, it improved to 29.5% (up from 28.2% in 2022) on the back of higher-margin “AI Transportable” products.

The U.S. segment (the “OSS segment”) posted a strong 35.6% gross margin in 2023.

Profitability Ups and Downs

After a profitable 2021 (net income of ~$2.3 million), OSS swung to losses in 2022 ($2.2 million) and 2023 ($6.7 million).

Notably, 2023’s loss includes one-time hits (e.g., a $5.6 million goodwill impairment, $1.7 million for a CEO transition). Adjusting for these, the company was near breakeven on a non-GAAP basis.

Recent Quarter Highlights

Q3 2024 Snapshot

Reported revenue of $13.7 million, flat compared to $13.75 million in Q3 of last year.

The U.S. segment delivered a 17.5% year-over-year gain, mainly from their defense-related sales.

European operations (Bressner) declined amid an economic slowdown.

A $6.1 million inventory write-down dragged the gross margin into the negative. Without this charge, margins would have been roughly 32%, up from 26.6% last year.

Net loss hit $6.8 million, versus a $3.6 million loss a year ago.

Management expects no further major write-downs and points to a strong backlog and growing “customer-funded development” revenue, indicating potential future production orders.Solid Balance Sheet

Cash & Liquidity

As of Q3 2024, OSS held $12.6 million in cash and short-term investments.

Working capital declined to $26.7 million from $35.6 million (mostly due to the inventory write-down).

Debt remains modest at around $2–3 million, leaving the company with a net cash position.

Path Forward

With low debt and decent cash reserves, OSS has a route to achieve profitability.

Management forecasts $15 million in Q4 2024 revenue. This could inch OSS closer to break-even, given expenses stay under control.

Growth Drivers

Specialized Edge Computing Niche

OSS’s focus on “Transportable AI ” solutions (rugged, high-performance computing in harsh environments) is an interesting niche as industries embrace on-site AI/ML processing.

Military, aerospace, autonomous vehicles, and industrials all need advanced computing power outside conventional data centers.

Innovative Product Pipeline

A new Gen 5 short-depth server (SDS) debuted in late 2023, featuring four powerful NVIDIA H100 GPUs in a compact 3U form factor.

The company also offers “ION Accelerator™” flash storage arrays and PCIe expansion systems for GPU and NVMe storage scalability. (although I am not sure how this solution solves for its bottlenecks…power and cooling, bandwidth, interoperability, etc.)

Market Expansion & Strategic Partnerships

The Bressner subsidiary serves European markets (despite current macro headwinds).

OSS works closely with Intel, NVIDIA, and defense contractors, often via “customer-funded development” projects. This ensures revenue during R&D and a built-in pipeline once full production begins.

Example deals include contracts with Leidos’ Dynetics unit ($2.5–3.5 million over three years) and FLYHT Aerospace ($6 million over five years).

OSS is also supplying rugged compute and switching modules for the U.S. Army’s Ground Vehicle Systems 360º Situational Awareness program.

Rising Industry Tailwinds

Defense modernization and autonomous vehicles that demand real-time AI at the edge.

Edge computing continues to expand across telecom, energy, and even into motorsports (Andretti Autosport uses OSS hardware for real-time analytics).

Challenges to the Turnaround

Competition

Larger defense-tech players like Mercury Systems and Curtiss-Wright, and smaller niche companies focused on rugged computing.

Staying ahead requires continuous R&D (large cost center).

Financial Risks

OSS remains unprofitable on a GAAP basis. Adjusted EBITDA was negative $8 million in the first nine months of 2024 (including the inventory write-down).

The $12.6 million in cash provides a cushion for now, but if the losses continue, OSS may have to make cuts or raise more capital (diluting existing shareholders)

Execution & Strategy Shifts

New management came in and cost $1.7 million. They also wrote down a bunch of old inventory… so they think the old stuff isn’t worth much anymore or they’re betting everything on AI instead.

The European segment (Bressner) underperformed, prompting a $5.6 million goodwill impairment.

Customer Concentration

Posted a sharp decline in revenue after losing a major media customer (concentration risk)

Gov. contracts can be inherently sticky but the sales cycle is long and the revenue is subject to political risk.

Macro & Geopolitical Uncertainties

Soft European demand has already hurt Bressner’s sales.

Economic downturns or supply chain hiccups could slow the roll-out of advanced computing hardware.

Financial Positioning & Shareholder Breakdown

Market Cap & Sales Multiple

At about $85 million in market capitalization (share price ~$4), OSS trades at 1.4–1.6x trailing 12-month revenue.

The company’s net cash position (~$10 million) nudges the EV/Sales ratio even lower.

If OSS returns to its $70+ million revenue run rate and edges closer to profitability, there could be room for multiple expansion.

Ownership Structure

Founders and directors hold roughly 25% of the shares, creating a strong alignment with common shareholders.

Another 25% is held by institutions, leaving ~50% with retail investors.

Stock Performance

Shares are up about 89% over the past year, reflecting optimism about AI Transportables and the company’s reset under new leadership.

The market will watch Q4 2024 revenue and margin performance closely to confirm that OSS can lean into its turnaround trajectory.

TL;DR

Pros:

Industry (AI edge markets) has high potential upside

OSS maintains strong partnerships with major defense contractors and leading tech players like Intel and NVIDIA

Low debt and decent cash

Cons:

Smaller player ($60 million revenue) when compared to larger industry peers.

Ongoing net losses and reliance on contract wins.

Potential volatility from macro forces and customer concentration.

Godel Terminal unites real-time market depth with institutional-grade research. Start free, or use code DRL for 30% off full access