SpaceX... What Does $135 Require You To Believe?

Using a Reverse DCF

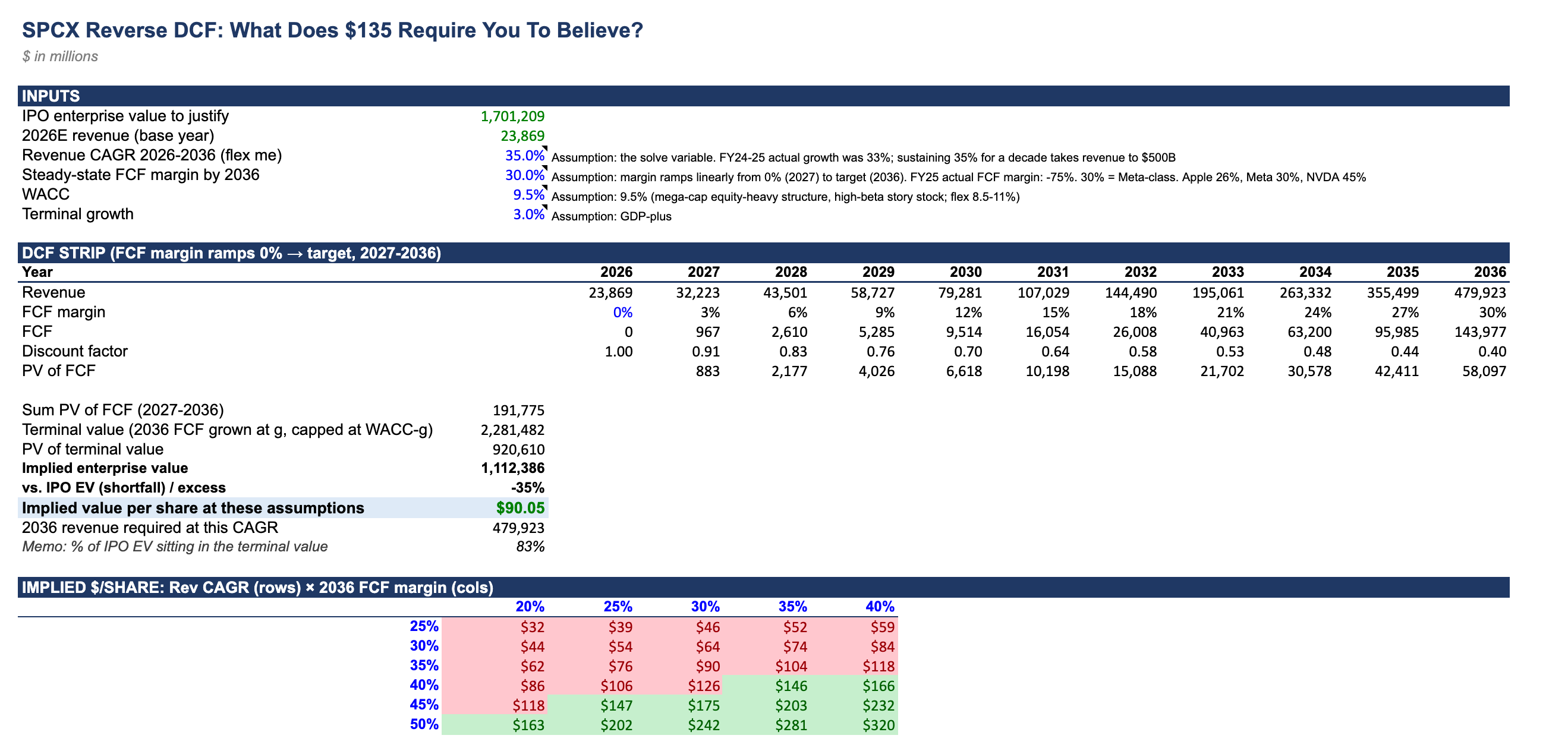

The most hotly anticipated IPO of all time.

Rather than argue about what SpaceX is worth I wanted to take a look at trying to understand what needs to be believed for $135 to be right.

Take the IPO enterprise value ($1.7T) and held the discounting machinery fixed.

9.5% WACC for a high-beta equity-heavy mega-cap

3% terminal growth

Solve for the two variables that actually drive getting to our answer: revenue growth and steady-state free cash flow margin.

The base case is rather aggressive (and rightfully so… the company is doing things that have never been done before). Assuming 35% revenue CAGR for ten straight years (FY24-25 actual growth was 33%, so this asks the company to accelerate off a $24B base and hold it for a decade, landing at $480B of 2036 revenue).

Assuming FCF margins ramp linearly from zero to 30% (Meta-class profitability, better than Apple) for a business that ran roughly -75% FCF margin in FY25. Zero out the near-term burn, booking $0 FCF in 2026 and positive cash from 2027. The real number is something like $(30)B a year. Every one of these choices flatters the IPO (but its a darling company, again, doing things that have never been done before.

Even on that floor, the model produces $90 a share (a 35% shortfall against the deal price). In order for you to get to the IPO $135, you need roughly 40%+ revenue CAGR at 30% margins, implying $700B+ of 2036 revenue (or 45-50% growth at more modest margins).

Around 83% of the implied EV sits in the terminal value. You cannot really underwrite this off of anything observable today. You are forced to underwrite to a time in 2036 where the assumption that it compounds at GDP plus forever after exists. Is that wrong? Not necessarily… (Starlink has unit economics and a launch monopoly that are certainly real). It does mean, however, that the investment case is almost entirely narrative duration risk and so any smaller changes in the discount rate or terminal assumptions swing your answer violently. There really appears to be no margin of safety against execution slippage in years 1-9.

Long story short… $135 isn’t a price you can defend with a DCF. It’s a price you pay if you believe SpaceX becomes one of the three or four most profitable companies in history. I would not bet against Elon and I am not bearish on SpaceX at all, in fact, I think if anyone can pull it off, it is likely Elon.